Joel Covelli on the details of Argentina’s Legal Drama

Maybe not as crazy as you thought

In an apparent step towards rapprochement with the international investment community, this past week the Argentine government announced that it would pay US$500mn in dollar denominated government bonds.

The payments are meant to resolve disputes filed by five multinational corporations (MNCs) at the World Banks’s International Center for the Settlement of Investment Disputes (ICSID).

Until last week, Argentina maintained a uniform policy of non-compliance with ICSID awards. This decision marked a major change of tact on the part of the Argentine government. Not coincidentally, the World Bank has just recently agreed to a US$3 billion lending program for health, education and rural development.

Argentina is understood by the international investment community as a deadbeat; a country that has stubbornly refused to meet debt obligations or court rulings. As a result, Argentina cannot raise capital on international markets—a crucial factor in the country’s skewed macroeconomic foundation.

But what if Argentina had a legitimate argument all along? What if the ICSID’s own review process acknowledged inconstancies in previous arbitration rulings, but had no power to overrule erroneous decisions?

A closer look at the cases and mechanisms suggest that there is more than what meets the eye.

A bit of context

ICSID is a form of international investment arbitration. First proposed at the World Bank’s annual meeting in Tokyo in 1964 and inaugurated in 1966, ICSID came about as a response to a wave of national expropriations. The goal of the program was to create a neutral forum for the resolution of investor-state disputes.

Consent to ICSID arbitration is usually provided by bilateral international investment treaties (BITs, thitherto referred to as treaties). These treaties provide a number of substantive provisions to protect investors from political and regulatory risks.

In what became known as the “el no de Tokyo”, Latin American countries initially rejected the ICSID, clinging instead to the Calvo Doctrine—first espoused by Argentine jurist Carlos Calvo in 1868 and informed by the region’s experience with gunboat diplomacy—which rejected special protection for international investors and required foreigners to bring their claims to domestic courts.

Play by house rules, essentially.

But by the 1980s, with much of the region plagued by stagnant growth, hyperinflation, and soaring public debt, the Calvo Doctrine was gradually swept away by neoliberalism. By 1997 only Brazil and Mexico were not party to ICSID.

The conclusion of the US-Argentina BIT treaty and Argentina’s entry into ICSID in 1994 was considered a milestone for the program because it marked a rupture with the Calvo Doctrine in its very country of origin.

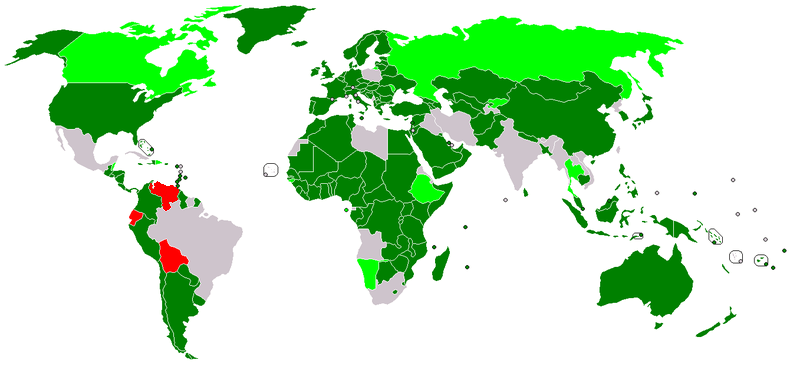

ICSID Members (Dark Green = ICSID in force; Light Green = ICSID signed, ratification pending; Red = Former members, withdrawn)

The Onslaught

However, over the next two decades, Argentina has had no fewer than 50 cases brought against, and refusing to pay award-creditors in a one of them.

It would be easy to interpret Argentina’s refusal to pay up as merely a part of the Kirchner’s general hostility towards the international investment community—highlighted by last year’s expropriation of YPF.

But, the story is more nuanced; a closer look reveals that Argentina has legitimate qualms with the validity of the decisions and the awards they have been ordered to pay.

Most of Argentina’s pending ICSID cases resulted from measures that altered tariff agreements that resulted in major losses for foreign utility providers following the country’s catastrophic economic crisis in 2001 that left 50 percent of the population below the poverty line.

In what became known collectively as the “Argentine gas cases” CMS Energy, Sempra Energy, Enron, and LG&E all brought cases before ICSID. These four cases were particularly controversial due to poor legal reasoning and inconsistent judgements.

Despite nearly the exact same fact patterns, the respective ICSID Tribunals reached substantially different conclusions.

In each of these cases Argentina relied on a Non Precluded Measures clause (NPM), in the US-Argentina BIT treaty, which provides exceptions to BIT for state measures that are deemed necessary for the “maintenance of public order” or the “protection of its own essential security interests”.

Essentially, Argentina argued a legal clause that allows for extraordinary actions when the mierda hits the fan domestically, as it most certainly did in 2001.

If 2001 does not count as a national crisis, just what does?

The CMS, Sempra, and Enron Tribunals relied on the customary international law (CIL) doctrine of necessity. This requires an emergency measure to be “the only means for a state to safeguard an essential interest against a grave and imminent peril”—rather than the NPM–—and awarded in favour of the investor.

Meanwhile, the LG&E Tribunal assessed both standards and found that Argentina satisfied both. This tribunal ruled in Argentina’s favour.

Demanding a Recount

ICSID does not have an appeals mechanism. But it does have an annulment process exclusively available to challenge the legitimacy of the Tribunal’s “process” and not the substantive correctness of the decisions.

Argentina brought the CMS, Enron and Sempra decisions to annulment. In Enron and CMS, the annulment committees found that the original rulings were not valid.

The committee creatively worked their rulings into ICSID’s limited grounds for annulment.

Meanwhile in the CMS annulment decision, the committee found that the tribunal made “manifest errors in law” by not applying the NPM clause (the mierda-fan clause Argentina had attempted to invoke).

Nevertheless it declared itself hamstrung to annul the decision based on ICSID’s limited annulment criteria: Again, this body does not have the authority to correct initial decisions.

Thus, Argentina was perversely asked to shell out US$133.2 million to CMS based on a decision declared by the World Bank’s own annulment committee to be based on bad law.

The Argentine gas cases provoked an outcry of criticism from the academic community. Perhaps the most cogent critique came from William Burke-White (who later served in the Obama administration).

The Argentine crisis cases rocked the ICSID system by exposing its unpreparedness to implement an appropriate or even a consistent standard of review for emergency measures taken by states.

The Argentine experience also highlighted the major drawbacks of not having a formal appeals process. ICSID must press forward to develop an appropriate and consistent standard of review state policy in response to crises and strongly consider the adaptation of a true appeals process.

Regional Reverberations

Naturally, the rulings emanating from the Argentine crisis provided fodder for leftist governments in the region, leading a number of them to discontinue ICSID support. Clearly countries such as Ecuador and Bolivia had other motivations for exiting ICSID beyond legitimate procedural criticisms of the Center.

In each of the countries, the governments unilaterally altered contracts leading to disputes being brought before ICSID. None of these measures came out of the emergency measures enacted akin to those of Argentina; rather they represent precisely the political risk that ICSID is meant to protect investors from.

“I told them the check was in the mail!”

The prospect of a UNASUR dispute settlement center realistically replacing ICSID’s role in the region is unlikely. Chile, Colombia and Peru would be unlikely to damage their business-friendly credentials by abandoning ICSID.

As for Argentina

Notably, two of the companies that Argentina has apparently settled with involve disputes with two water service providers, French Vivendi and US-based Azurix. Non-payment in these cases is perceived as particularly offensive to international investors because they are pre-crisis disputes. Argentina has also offered Repsol US$1.5 billion for last year’s expropriation.

By also compensating Blue Ridge Investments–who purchased CMS’s interest in the award described above– the Argentine government has demonstrated a willingness to take one on the chin in order to convince for the US to jettison their policy of voting against World Bank lending to Argentina.

While this is a conciliatory step, don’t expect Argentina to change its stance against the “vulture capitalists”. In fact the moves could also be an attempt to illicit US government support for Argentina’s ongoing US court battle with hold-out bond holders.

And thus, the saga continues.

Too much drama!

Joel Covelli is a Latin America specialist currently completing a dual degree program in Latin American Studies at Johns Hopkins SAIS and law at the University of Ottawa

Also by Joel

The Roar of a Nation

No Se Mancha Covers Argentina

Argentina: Wrong Way on a One Way Track? (Alex Rosen)

What Greece Can Learn from Argentina (Samuel George)

Argentina Censored – But Does it Matter? (Cornelius Fleischhaker)