By Political economist and Latin America-specialist Samuel George

How infrastructure can spark growth

*This post is an excerpt from an upcoming working paper entitled “Five Steps to Kickstart Brazil” coauthored with Cornelius Fleischhaker (UPDATE: The study is now available HERE)

From unpaved streets in the northeast to the overburdened ports of Santos, Brazil’s infrastructure deficit is ubiquitous and costly. Brazilian fields produce grain twice as fast as those elsewhere but getting that grain to port can cost almost half its value. Meanwhile, vast mineral deposits remain buried deep within the earth (and vast numbers of people remain buried deep in São Paulo’s traffic) for want of better transportation.

Statistics support these anecdotes. Despite assuming the mantle as the world’s sixth largest economy, the 2013-2014 World Economic Competitiveness Report found Brazil to rank 71st globally in infrastructure. At roughly 2.45 percent of GDP—only slightly above the estimated two percent required simply to maintain the existing infrastructure stock—investment in Brazilian infrastructure is below the emerging market average and a far cry from major economies, which typically spend five to seven percent of GDP annually on infrastructure

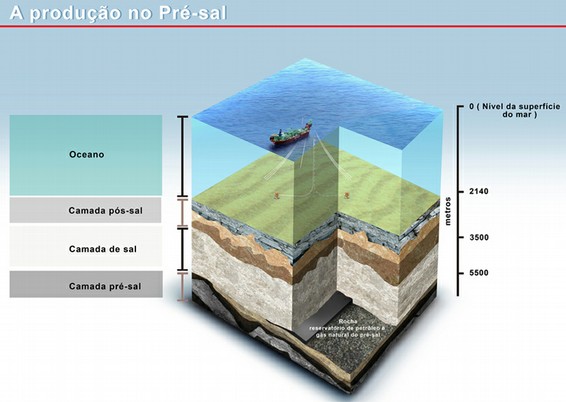

Not only does this deficit hamper growth in established sectors, it prevents the country from fully exploiting new ones as well. For example, the 2007 discovery of tremendous deep-sea oil fields off the Brazilian coast increased the country’s probable oil reserves from 20 billion barrels to well over 50 billion barrels.

But having the oil is one thing. Extracting it has proven quite another. Pre-sal oil excavation presents significant engineering challenges and requires advanced infrastructure that could cost upwards of US$400 billion. In her first administration, President Dilma sought to stimulate Brazilian production by building these inputs domestically. To this end, her government implemented local-content laws that require oil extraction to be conducted with machinery built in Brazil.

In theory, such a stimulus to production would create thousands of domestic jobs while spreading the wealth from any oil boom. In practice, it has delayed the country’s access to its hydrocarbon trove, and thus—ironically—denied Brasilia a degree of fiscal slack that could be used on other infrastructure and education project.

…this is not gonna be easy

The good news is that addressing infrastructure can provide large gains.

Crucially, Brazil must focus on a long-term strategy. Projects associated with the recent World Cup and the upcoming Summer Olympic Games provide, at best, short term solutions. Meanwhile, chunks of the government’s ‘PAC II’ US$885 billion infrastructure investment package are earmarked for pre-existing problems, such as housing. Such investment is crucial, but alone it cannot pave the way for future growth.

A long-term infrastructure plan that will kick-start growth should focus on transportation—and not just roads. A 2013 PWC study highlights the importance of freights and waterways as more efficient than roads for transporting goods in Brazil. With over 17,000 miles of navigable water, moving 1000 tons one kilometer by ship is roughly a quarter of the cost of moving it by highway.

Yet, with most of these waterway set deep within Brazil’s underdeveloped northeast, just one percent of the country’s freight volume is shipped this way. Developing waterway infrastructure could both improve transport efficiency and facilitate economic inclusion–two trends that would have a positive effect on growth.

Modernized ports can also expand Brazil’s ability to export abroad. Prior to suffering a dramatic bankruptcy, Brazilian entrepreneur Eike Batista dreamed of a super-port that combined expanded capacity with on-site production facilities that would ensure Brazil would play a role in processing—as opposed to simply exporting—commodities. Batista may no longer be in a position to execute such a strategy, but it is not a bad one.

The key question is who will finance these projects.

Currently, the Banco Nacional de Desenvolvimento Economico e Social (BNDES), a state-owned development bank, plays a major (and expanding) role in underwriting infrastructure investment.

However, with a loan portfolio value that eclipses that of the entire World Bank, BNDES may actually be crowding out private investment by creating an atmosphere of artificially low yields. Meanwhile, some have questioned whether close ties to power are required to be awarded subsidized BNDES loans.

These deterrents to private investment are concerning as, simply put, the state cannot do it alone. BNDES has already proved incapable of single-handedly closing Brazil’s infrastructure deficit. Given forthcoming fiscal constraints, the private sector must join forces with the state.

Fortunately, investors worldwide have shown keen interest in Brazil, as demonstrated by continued FDI inflows. Securing this investment will require an improved framework for public-private partnerships and the removal of procedural burdens that slow projects (the infamous custo Brasil).

If a second Rousseff administration can attract and manage high quality, guided infrastructure investment, Brazil can clearly expand it productivity capacity, generating ample opportunities for growth.

Samuel George is a Latin America specialist working in Washington DC. Check out his external work HERE, and his work for the blog HERE. On Twitter @SamuelGeorge76

Stay tuned for the upcoming working paper Five Steps to Kickstart Brazil, coauthored with Cornelius Fleischhaker and based on the Financial Times editorial of the same name.

Pingback: Brazilian Infrastructure: The Good, the Bad, and the Opportunity | Denmark Brazil