Cornelius Fleischhaker and Samuel George on Brazil’s macroeconomic challenges

Inflation has reemerged as a concern in Brazil

Last week, we took a look at some of the fiscal issues that recently-appointed Finance Minister Joaquim Levy will face in 2015. Yet while fiscal policy may be at the heart of the current Brazilian malaise, the country also faces important monetary challenges.

For the moment, it appears that current Central Bank Governor Alexandre Antônio Tombini will maintain his post at least to start the second Dilma administration. He will likely struggle both to reassert his independence, and to get Brazil’s macroeconomic house back in order.

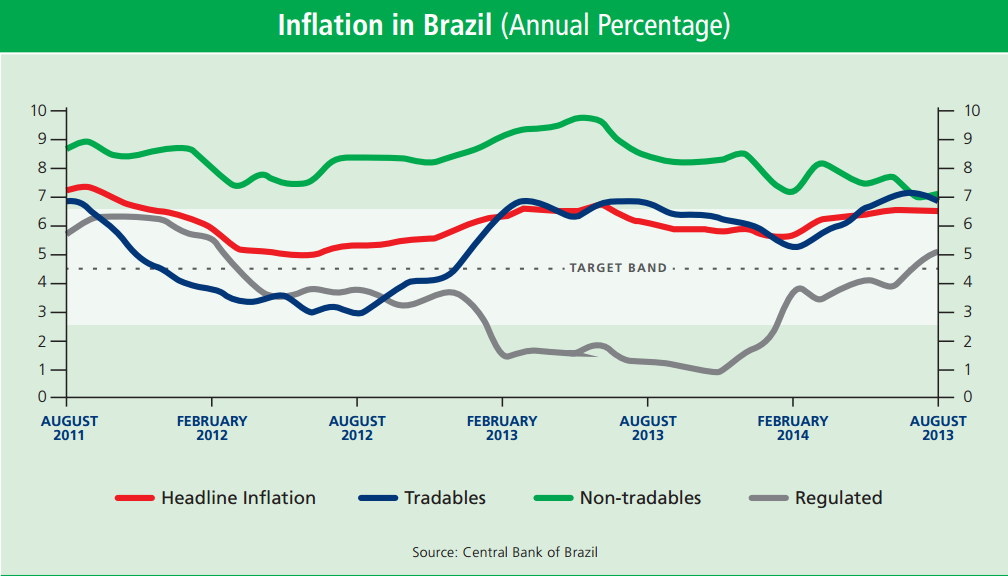

At 6.6 percent, inflation is currently above the country’s upper target-rate limit and has been near it for several years, creating a perception of inflation tolerance and consequently de-anchoring expectations.

The bad news is that inflationary pressures will likely remain pronounced over the coming months, given the recent depreciation of the real (roughly ten percent over the past two months) and the need to further raise domestic energy prices to bring them in line with the cost of production. Thus, the 4.5 percent inflation target will likely remain out of reach in the near term, even if the Central Bank continues to raise interest rates.

Increasing macroeconomic instability has a negative drag on growth. Inflation translates to constant appreciation pressure on the real exchange rate as the prices of Brazilian goods and services rise faster than elsewhere. This hampers the competitiveness of Brazilian firms, which in turn stifles growth.

Furthermore, once inflation takes hold, the medicine can do as much as harm as the ailment. In an effort to curtail rising prices, Brasília sets prices artificially low on goods administered by the government such as fuel, electricity and public transportation. This create significant distortions in the economy. For example, the price freeze on fuel in recent years has challenged Petrobras’ ability to invest in oil exploration and infrastructure, while at the same time severely damaging the once booming sugarcane ethanol industry.

Most importantly, inflation always hurts the poor who depend on the purchasing power of their earnings to make ends meet. The recent uptick in extreme poverty is a very concerning sign in this context.

Setting a New Course

Just as on the fiscal front, the first step to restore stability in the medium-term is to recover credibility. While inflation may continue to run above target in the near-term, the authorities must send a strong signal that it will be controlled in a realistic timeframe through an appropriate mix of monetary and fiscal policies, and not through price fixes—a strategy that has previously proven ineffective in Brazil.

The Central Bank should be guaranteed the operational autonomy to bring inflation back to target in the medium term. Fiscal policy, quasi-fiscal operations through state-owned banks (especially BNDES), and government intervention in the credit market should support the inflation-control effort rather than contradicting it, as has been the case in recent years.

Controlling inflation without artificially setting prices will benefit growth in a number of ways. Primarily, it would reduce the uncertainty under which both investors and regular Joãos make decisions. Investors will be more willing to invest in productive assets such as ethanol or electricity if they can be assured that government intervention will not wash away their returns. Middle class citizens will be better positioned to plan for the future if they know the purchasing power of their salaries will be protected.

Secondly, controlling inflation would help address the eternal dilemma of the Brazilian economy: Very low savings at the world’s highest interest rates (in mid-2014, the average lending rate for non-directed credit was more than 40 percent).

Both of these tendencies stem in part from the threat of inflation. There is little incentive to save if that effort can erased by a bout of inflation. Meanwhile, the high interest rates reflect a risk premium associated with mistrust in the government’s ability to hit inflation targets.

If the new Rousseff Administration can reaffirm Central Bank autonomy while reigning in government spending, inflation will come down. Over the long run, Brazil’s absurdly high interest rates would follow suit. But such resulted require prudent macroeconomic management; they cannot be achieved through shortcuts.

Brazil fought hard for macroeconomic stability in the 1990s. That effort must not go to waste.

Kickstarting Brazil: Check out the video!

This post contains excerpts from the study Five Steps to Kickstart Brazil composed by the authors.

Samuel George is a Latin America specialist working in Washington-DC. On twitter @SamuelGeorge76

Cornelius Fleischhaker specializes on Brazil at the World Bank. The opinions expressed here are his own and do not reflect those of the World Bank. On twitter @tiocornelio

Pingback: GED Blog | Brazil - A Country of Buts - GED Blog