The Venezuelan Bolivar Fuerte: Not as fuerte as it used to be

Venezuelan President Hugo Chávez returned to Caracas on February 18th after two months of medical treatment in Cuba. If he took any Venezuelan Bolivares there with him they are now worth only two-thirds of their value when he left.

On Friday, February 8th, while many Venezuelans dropped their attention on the economy to enjoy carnival, the government dropped the exchange rate from 4.3 Bolivares to the dollar down to 6.3 – a devaluation of 32 percent. The government also eliminated a second official exchange rate maintained by the Central Bank of 5.3 Bolivares per dollar, unifying the official rates at 6.3.

Given that high inflation has led to a continuously increasing overvaluation of the Venezuelan currency, a devaluation had been widely expected for this year, but many observers thought this unpopular step would be delayed, until after a possible election to replace the Mr. Chávez, who many suspect may be unable continue as president. Most economists agree that a devaluation was necessary to bring the currency more in line with market fundamentals. For all we know, the Bolivar is still significantly overvalued with greenbacks trading for more than 20 Bolivares on the streets of Caracas.

A Bitter Pill for a Very Sick Country

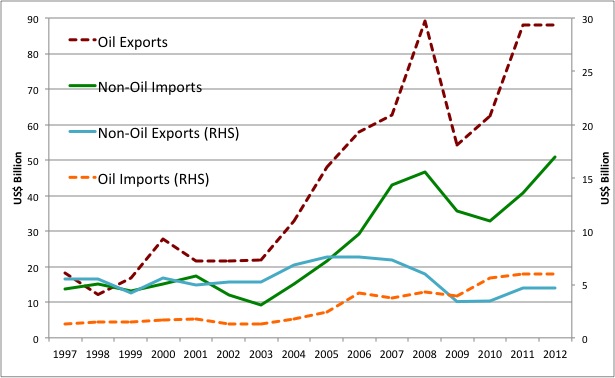

The devaluation will have several positive effects on the Venezuelan economy. The devalued Bolivar will help the country balance its current account, as the diminished buying power of the Bolivar will suppress imports, which have been growing rapidly. On the other hand, however, this will lead to fewer imported goods available to Venezuela consumers at higher domestic prices, which will only increase inflation and scarcity – two factors that are already placing significant stress on Venezuelan consumers. Even before the devaluation, scarcity as reported by the Venezuelan Central Bank, had reached a new record.

Oil up – all else down

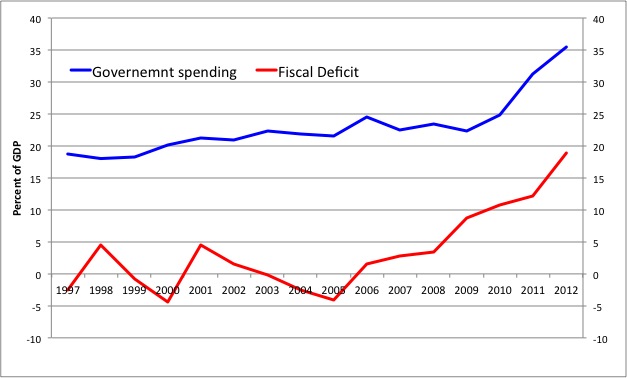

However, the primary reason for the government to pursue devaluation is the easing effect it will have on public finances. Since Venezuela’s budget is financed first and foremost through petroleum exports, moving from 4.3 to 6.3 Bolivares per dollar gives the government two extra Bolivares for each petrodollar earned. With oil exports estimated at around US$85 billion a year, this has the potential to significantly improve the budget deficit, which reached a devastating 17 percent of GDP in 2012. Had this additional income been available last year, it would have nearly cut the deficit in half. Government spending grew rapidly last year, owing to election won by Mr. Chávez in October. Given the high probability of a new presidential election this year, the government might be unwilling to tighten its belt just yet – hence the preference for devaluation now, hopefully months before any forthcoming election.

Hey Big Spender…

More than a placebo effect?

Nevertheless, despite these positive effects, the devaluation changes very little about the underlying economic problems facing Venezuela. Inflation came in at roughly 21 percent last year. This will further deteriorate as the 32 percent devaluation will make imported goods significantly more pricy overnight. The pass-through effect (the effect of higher import prices on the overall price level) will be strong, as Venezuela has become heavily dependent on imports of all kinds as the government’s mismanagement of the economy has led to a collapse of economic activity in the non-oil sector.

Even the all important oil sector has suffered as the government has strangled the state-owned PDVSA’s budget and diverted funds away from investment and maintenance. Consequently, Venezuela’s oil production has been stagnant for more than a decade, even though the country sits on as much as 300 billion barrels in reserve. Last year, Venezuela had to go as far as to import large quantities of gasoline and diesel from the United States after a series of major accidents at its refineries and other installations, attributed to poor maintenance reduced refining capacity. Similar problems have led to frequent blackouts in the most energy rich county in the region.

While all the above are serious economic ills, they only compete for second place in the list of worries of most Venezuelans behind the rise of violent crime. The murder rate has reached 73 homicides per 100,000 people, worse than even the deadliest Mexican States and more than double that of neighboring Colombia.

Who’s getting better – who’s getting worse?

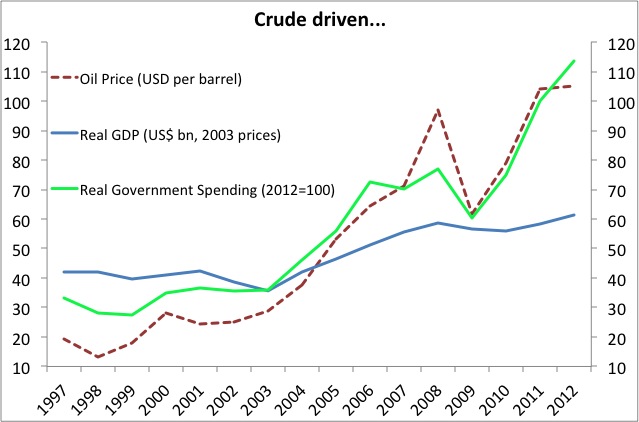

While we don’t know much about the illness Hugo Chávez may or may not be recovering from, we do know a lot about the poor health of the Venezuelan economy. However we also know, that the Venezuelan economy has a strong lifeline: the price of oil. As long as oil prices stay strong, the Chávez economy will manage to survive – which is more than we can say about Mr. Chávez himself at this point.

Cornelius Fleischhaker is currently a Research Analyst at the International Monetary Fund. The opinions expressed in the post are those of the author only and should not be attributed to the International Monetary Fund.

Pingback: Three (not so simple) steps for curing the Venezuelan economy | No Se Mancha