Energy and financial analyst (and wannabe Chilango) Jesse Rogers on cold feet in Latin America’s strongest economies

Will tapering weigh on the peso?

The prospect of a US base rate hike next spring has given finance ministers in some of Latin America’s best-managed economies a severe case of escalofrios, or market jitters, despite a sustained recovery in capital flows to the region.

Some officials fear such a rise in US interest rates could set off a new wave of capital flight, falling currencies, and inflation.

“Everyone is getting prepared,” Mauricio Cardenas, Colombia’s Finance Minister, said in an interview with the Wall Street Journal.

In May 2013, the mere suggestion that the Federal Reserve would “taper”, or reduce the scale of its US$85 billion monthly bond-buying program, sent markets into a tizzy.

Interest rates in Brazil, Mexico, Chile, Colombia, and Peru—Latin America’s largest economies, by market capitalization—rose almost 150 percent in the ten days following the Fed’s tapering comments as frenzied investors dumped Latin American stocks and bonds in anticipation of higher returns in the US.

While tapering fears proved premature—the Fed would not begin to pare back bond purchases until January 2014—the damage in these five economies was palpable.

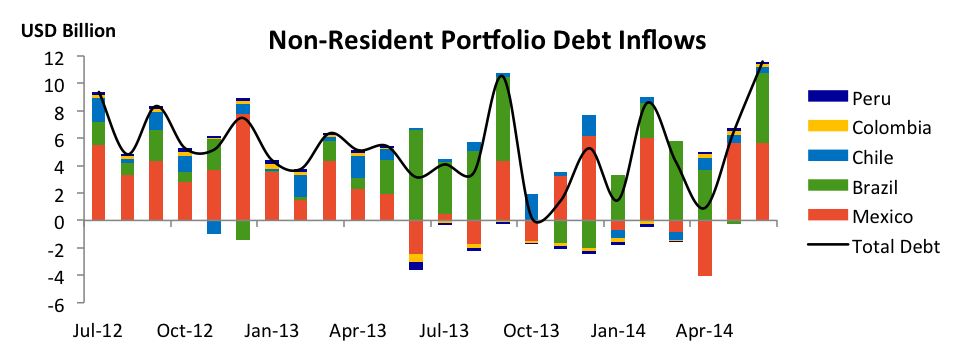

In just one month, investors withdrew US$7.6 billion in equity shares, nearly wiping out a cumulative US$11 billion in equity inflows from January to April 2013. Debt outflows in May 2013 totaled another US$7.3 billion, with the exception of Brazil (purchases of Brazilian securities actually increased over the prior month).

Source: Central Banks , EPFR, IIF

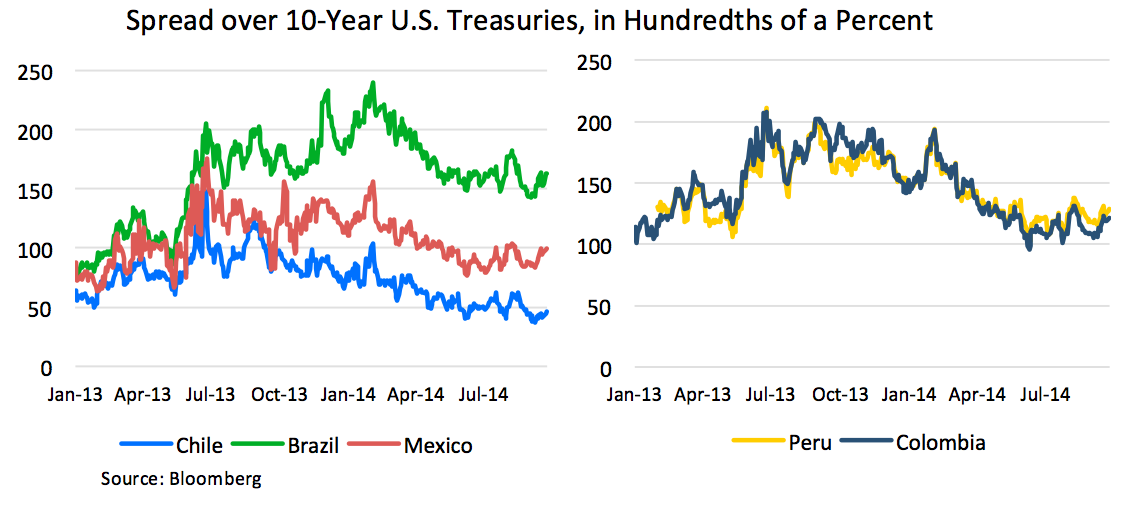

Though borrowing costs (as measured by the spread in basis points, or hundredths of a percent, over US Ten-year Treasury yields) are now back to pre-May 2013 lows, Colombia, for one, is not taking any chances.

Finance Minister Cardenas announced in mid-September that the country may tap international bond markets before the end of this year for part of its US$3 billion sovereign debt issue, originally planned for 2015. Cardenas is also hoping that greater local appetite for Colombian debt will prevent another race for the exits when US rates do rise.

Yet there are at least three reasons why the impact of the Fed’s spring rate hike in Latin America will likely be milder than 2013’s “taper tantrum”:

First, there is an argument to be made that investors will be more discerning this time around.

According to this outlook, strong macro fundamentals will ward off capital flight, leaving countries that are large borrowers or suffer from either rising inflation or low growth in investors’ crosshairs.

By these marks, Mexico, Chile, Colombia, and Peru appear to be doing quite nicely, and while Brazil’s current bout with stagflation is indeed alarming, it has kept net borrowing as a share of GDP at or below 3 percent, widely regarded by economists as the demarcation line for debt sustainability.

Second, benchmark stock indices and most currencies are still below pre-2013 highs.

While financial conditions have eased since the summer of 2013, the argument goes, once-overpriced securities have now experienced a “correction”. In other words, yesterday’s fall makes them less likely to decline today.

Finally, the Fed is not the only game in town.

Though investors are likely to return money to the U.S. as interest rates rise, the Euro-slinging ECB is about to embark on a quantitative easing program of its own, while monetary stimulus in Japan will also free up capital in search of higher yields.

Although winter, or invierno, as Mr. Cardenas might put it, is indeed coming, Latin America’s five most financially integrated economies should make it through with a breeze.

The view from the Colombian stock market? Not so bad…

Jesse Rogers is an energy analyst focusing on natural gas markets in Latin America. He previously worked as a finance and politics reporter for Impremedia and as a research assistant for Mexico City’s Centro de Investigación y Docencia Económicas (CIDE).

esta posible limpiarse

colombia is intriguing

i’m going to brazil

Thanks for calming the escalofrios!

Very interesting blog. The kind of clearly written analysis of complex issues that one finds in the NYTimes’ business and finance columnists besides Paul Krugman. Thanks!

No creo que mexico se vea amenazada por los flujos de efectivo