By Jesse Rogers of Moody’s Analytics

Heating up…

Brazil may be the country of tomorrow, but when it comes to Latin America’s energy security, Chile is having its moment in the sun.

The mining powerhouse is emerging as one of the world’s most dynamic markets for solar power, thanks to its high solar isolation, competitive policy framework, and the high relative cost of conventional power.

Advocates of solar power have long looked to Chile as the next frontier for cost-effective solar generation. Across Chile’s vast Atacama desert, solar isolation – a measure of the intensity of solar radiation per unit of surface area – is among the highest in the world.

But until recently, the prospect of large-scale solar power was little more than a pipe dream. The high cost of solar panels and round-the-clock demand from the country’s outsized mining industry prevented solar from emerging as a viable alternative to large-scale hydro, natural gas, and diesel generation.

However, the economics of solar power are quickly breaking in Chile’s way. New innovations and anemic growth in the European Union – the world’s largest solar market – have pushed down prices for solar panels, so much so that solar developers in Chile are now outbidding conventional utilities in auctions for new energy supply.

In January, Spanish energy giant Abnegoa won a contract to supply electricity to nearly 350,000 homes on Chile’s Central Interconnected Grid, or SIC. The strike price – 11.5 cents per kilowatt-hour – is almost a third cheaper than the grid’s average generation price.

Improved access to Chile’s transmission infrastructure, a product of President Bachelet’s new energy policy, has given solar a helping hand. But in contrast to solar projects in the European Union, Chile’s solar developers receive no subsidies or feed-in tariffs. This makes Abnegoa’s winning bid all the more impressive.

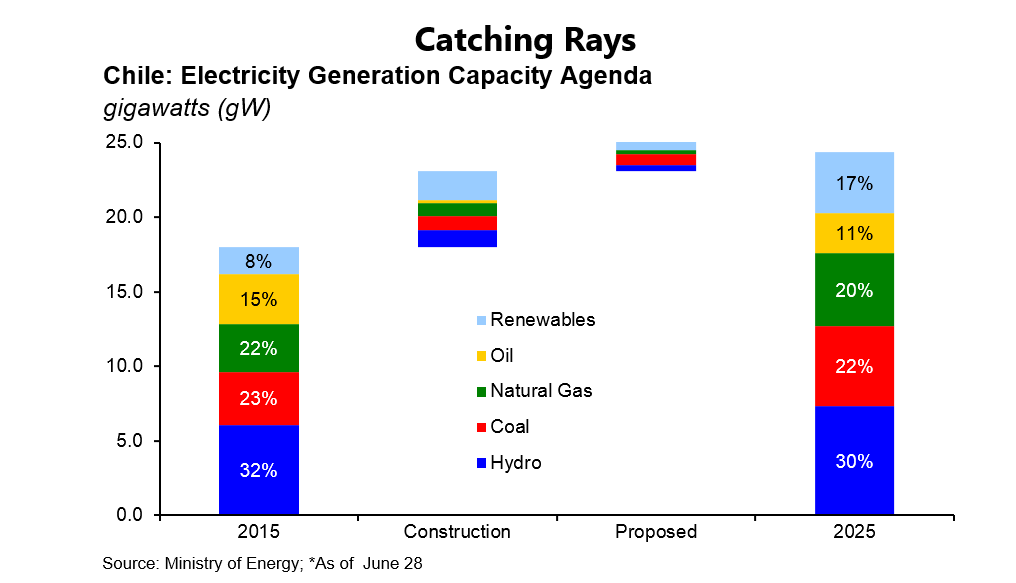

Over the past year and a half, the installed capacity of solar power has shot up from just 4 megawatts (MW) to over 200 MW, according to figures from Chile’s ministry of energy. Projects currently under construction will add an additional 1900 MW over the next twelve months. This compares to just 15 MW of installed capacity in Brazil and around 100 MW in Mexico.

Solar is also flexing its rays on Chile’s northern grid, which supplies power to most of the country’s large mining companies. New technologies to store solar energy and release it during times of low insolation are making it an increasingly attractive proposition for power-thirsty mining operations.

But despite Chile’s lead, solar power will make only a small dent in the country’s future energy needs.

The mining powerhouse is one of the most energy intensive economies in the 34-member Organisation for Economic Co-Operation and Development, a group of mostly developed nations. According to the OECD, for every one percentage point rise in Chile’s GDP, the country’s electricity supply must rise by 1.5 percent.

Going by the ministry of energy’s current projections, this means that Chile will need to double its installed capacity over the next ten years to live up to its potential, or long run rate of economic growth. This will entail the adding of up to 15 gigawatts of new generation.

Doing so won’t be easy. Chile’s rowdy environmentalist movement has made it difficult to envision new generation capacity of nearly any sort.

Beset by protests, former president Sebastian Sebastian Piñera called off energy company GDF Suez’ 540 MW Barrancones coal project in 2011. Meanwhile, current president Michelle Bachellet declared Endesa’s 2,750 MW HidroAysén project “not viable” two months in to her presidential term.

While new innovations, favorable access to financing, and natural bounty will keep Chile on the leading edge of Latin America’s solar wave, stronger leadership is needed to balance larger projects with politically palatable but lower capacity solar, wind, and small hydro installations.

Given slowing growth and the president’s latest approval numbers, the road forward won’t be without curves.

Jesse Rogers is an economist with Moody’s Analytics covering energy markets and Latin America.