…and what it means for Latin America

The biblical King Solomon might not have been a commodity trader but he knew this much:

There is a time for everything, and a season for every activity under the heavens: a time to be born and a time to die, a time to plant and a time to uproot, a time to kill and a time to heal, a time to tear down and a time to build (Eclesiastes 3:1-3)

Similarly some commodity traders have reached the conclusion that there was a time to invest in commodities but now this time has passed.

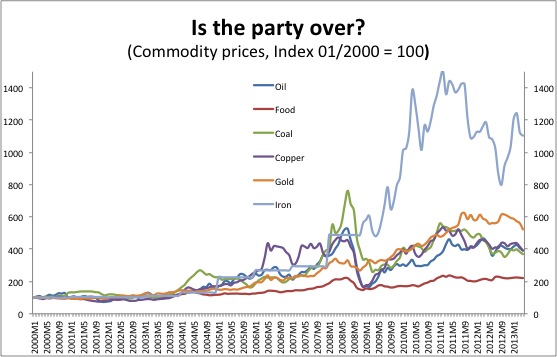

For roughly a decade begging in the early 2000s commodity prices knew really only one direction: Up. An investor betting on oil, iron, gold or silver in 2000 would have seen their investment grow by several hundred percent in real terms (accounting for inflation) over ten years. Many commodities reached a frenetic peak in 2008 right before the Lehman bust. Even while they fell sharply in late 2008 and early 2009, they bounced back quickly in the following years.

Price trends over the last few years are somewhat inconclusive but there appears to be strong evidence that the commodity super cycle of the 2000s is indeed over and that the overall trend going forward will be downward. To come to this conclusion we need to understand some basic workings of the commodity markets.

Resource reliance: A downward spiral?

Commodity markets 101

It will come to little surprise, that, as in other markets, prices in the commodity markets are determined by supply and demand. However supply and demand in commodity markets have a number of interesting features. Generally, there is a long-term trend, which is fairly inelastic in the short run, meaning that quantities demanded and supplied will not respond much as an immediate reaction to changes in price.

High oil prices might lead Americans to switch to fuel efficient cars over time which will reduce oil consumption in the long run, but a US$5 per barrel rise in the oil price today will not lead to a significant reduction in fuel consumption next week. Similarly, high prices will lead to more investment in mines and oil wells, which will increase supply in the long run, but these projects can easily take a decade to come online.

So a decision taken today to invest (or not) driven by high (or low) prices will only result in greater supply in the mid-2020s.

Hence, while the underlying trends of supply and demand are usually moving slow and steady, daily prices are often determined by shocks: short-term disruptions in supply and demand.

A particular feature of commodity markets is that these shocks on supply as well as demand are almost always negative (resulting in a lower quantity supplied or demanded). Such a negative shock, say the unrest in Libya in 2011 disrupting oil production or heavy rain in Colombia reducing the coffee crop, will lead to lower than expected supply and higher prices. It is hard to imaging a positive supply shock (“El Dorado finally found!”), which would lead to an unexpected increase in supply and falling prices (in agricultural commodities, a better than expected harvest is an example of a limited positive supply shock).

Similarly on the demand side, surprises tend to be mostly on the downside. Demand for most commodities is driven by economic activity hence a surprise recession (along the lines of the Lehman shock) can send commodity prices on tailspin. A positive demand shock on the other hand would require an unexpected boom, which curiously does not seem to happen all that often.

Where we are now

So let’s talk about where we are right now. In terms shocks, we live in a world of great uncertainty where negative supply shocks leading to higher prices seem to be just as conceivable as negative demand shocks leading to lower prices.

Where do we go from here?

The case for falling commodity prices in the medium and long term however is based more on the underlying structural features. As could be expected, the commodity boom of the 2000s has led to plenty of investment and innovation on the supply side, most notably in the area of oil and gas.

The dragon in the room is always China. The baseline assumption is that growth in China is slowing down and is becoming less commodity-intensive, which by itself should exhort downward pressure on commodity prices. Yet, surprises on Chinese growth and commodity demand seem very much possible and as always they are asymmetrically on the downside.

Rumors of a looming crisis, financial or other, have persisted for years and are still alive today, and just because it hasn’t happened so far doesn’t mean it never will. Even if a dramatic crisis does not materialize, a soft landing and with a shift from commodity-intensive investment to less commodity intensive consumption should still make us bearish on the raw materials that have been feeding the Chinese boom such as copper, coal and iron ore.

Of Booms and Busts: In the 16th century, silver made the Bolivian city of Potosi one of the richest in the world

On the supply side, things look very different depending on which commodities we chose to focus on. For agricultural commodities, recent studies indicate that supply might actually have a hard time keeping up with demand, which would mean high prices for many years to come. On the non-edible stuff there is a general trend for supply to increase at a faster pace than demand. The period of high prices has induced investment in mining, drilling and fracking many places, most importantly Gringolandia.

As discussed, investments in mines and oil rigs take a long time to yield output so the price rises between 2003 and 2008 might be showing up as new supply just about now. We have already seen how this has depressed natural gas prices in the western hemisphere (as gas is not easy to transport, natural gas markets are segmented).

What does it all mean for Latin America?

Many Latin American economies remain commodity dependent and generally have become more so in recent years as commodity prices provided a strong incentive to increase output in extractive industries often at the price of losing competitiveness in other areas.

The share of raw materials in total exports has grown significantly in countries such as Brazil, Peru and Colombia. Commodity dependence in Latin America knows no political camps; members of the pro-market Pacific Alliance such as Chile, Peru and Colombia are just as much affected as ALBA countries like Ecuador and Venezuela.

While the commodity effect is great in all of these countries, it affects them through different channels. In Peru or Colombia, resource wealth has attracted foreign investment, which in turn resulted in higher growth and improved government finances.

In Venezuela but also Chile, rising commodity prices have a direct effect on government finances through government ownership of the petroleum and (most of) the copper industry respectively. Maintaining economic growth and sustainable government finances as the tailwinds of high commodity prices recede will be a key challenge for all of these economies.

Recently by Cornelius

Istanbul & São Paulo: A World Apart, a World United

The Sick Man of the Amazon – The Debate Over Brazil

Habemus Paco

Pingback: Why the commodity super cycle is probably over… « Economics Info

Pingback: Pumas, ALBA, Mercosur, and the Supposed South American Split | No Se Mancha

Pingback: TPP and the Pacific Alliance: Two Visions of Asia-Latin America Trade | No Se Mancha

Pingback: Pimp My Rainforest | No Se Mancha

Pingback: Scratching the Surface: Commodities in Post-Boom South America | No Se Mancha