Latin American trade and investment analyst Theodore Kahn on Premier Xi’s Visit to Mexico

Competitors? Companions? Changing Dynamics in Mexican-Chinese Relations

Chinese Premier Xi Jinping arrives in Mexico City today for a two-day visit with Mexican President Enrique Peña Nieto. The meeting, coming in both leaders’ first year, has been billed as a chance to “re-launch” bilateral relations. After a decade of distant, wary relations, due primarily to the perception of zero-sum competition between the two economies, such a re-launch be a positive development.

So what would a cooperative Chino-Mexican relationship look like? And is it possible to achieve?

Competition is the name of the game

China’s accession to the World Trade Organization in 2001 sent a shiver down the spine of Mexican industry. With a seemingly endless supply of cheap labor and arsenal of industrial policies, the Chinese juggernaut appeared to be a direct threat to Mexican producers’ privileged position to the US market – not to mention a threat to the Mexican firm’s domestic business.

Indeed, China’s share of US imports increased from around 8 percent in 2001 to almost 20 percent by 2011 – much of this gain likely at the expense of Mexican producers, whose market share in the US stagnated over that period. At home in Mexico, a flood of Chinese imports competed directly with domestic products – battles that Chinese manufacturers usually won. Reports of factory closings, demands for protection against Chinese imports, and concerns over the ever-expanding trade deficit were mainstays in the Mexican media throughout the mid-2000s.

The global financial crisis of 2008 hit pummeled the Mexican economy, while much of Latin America – shielded, incidentally, by strong Chinese demand for its natural resources – skated through relatively unscathed. It seemed that Mexico, with its reliance on a slumping US market, facing the scourge of drug-related violence, and the poor luck to be competing head-on with explosive Chinese industry, had found itself in the slow lane of a two-speed region.

Fast-forward two years, and the roles have reversed.

By early 2013, Mexico was being hailed as the new emerging market champion. Blue-chip companies in industries ranging from automobiles to electronics to medical equipment made plans to locate production in Mexico, taking advantage of its new-found dynamism and proximity to the US.

In a clear indication of turning tables, Chrysler announced it would produce its Fiat 500 model in Mexico for export to (gasp) China. Felipe Calderon, Mexico’s President at the time, admitted “we always thought it would be the other way around.”

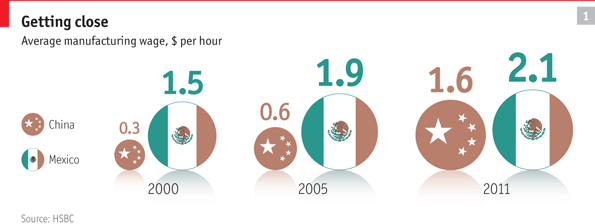

How was the script so thoroughly flipped? To begin with, rising salaries have eroded China’s wage differential with Mexico, which stood at nearly 200 percent when China joined the WTO in 2001. Meanwhile, the recovery in oil prices since the global financial crisis has given Mexico an additional competitive advantage in the US market.

No longer minding the gap

On the political front, the election of Enrique Peña Nieto in July 2012 raised expectations that major structural reforms were in the works. This expectation seemed to be validated when the Mexican Congress approved a labor reform bill under outgoing President Felipe Calderon, and Peña Nieto introduced major overhauls of competition policy and the banking sector in rapid succession.

So is Mexico really “the new China”?

Some caution is in order here. The story of Mexico’s resurgent competiveness vis-à-vis China has largely been about the convergence of labor costs and some anecdotal evidence of companies moving production in Mexico to better serve the US (and in some cases South American) markets – the so-called “near-shoring” phenomenon.

This is a very reductionist view of competitiveness. For foreign investors, labor and transport costs are obviously a major concern. From the perspective of national policymakers, domestic firms, and workers, however, it is other elements of competitiveness – such as productivity, technological upgrading, and innovation capacity that really matter.

In these facets of competitiveness, China still blows Mexico out of the agua. The auto industry provides a good example. In Mexico, foreign carmakers such as Ford, Volkswagen, and Nissan produce vehicles using a high proportion of imported technology, services, and parts. The production chains that do exist within Mexico tend to be populated by other multinationals – major auto parts producers such as Michigan-based Delpi and European firms Valeo and Bosch are both present in Mexico.

The situation in China is different. True, the leading North American, European, and Japanese brands all produce cars in China, but they increasingly compete with indigenous firms making their own models. In some cases these companies are partly state-owned, but not all. Firms like Geely and Chery have consistently gained market share in China and are even expanding aggressively abroad, above all in emerging markets where their price points are a big draw for middle-class consumers. Chinese companies enjoy cost advantages as large as 35 percent over developed country car makers.

No Mexican original manufacturer can claim this type of global ambition, because there is no Mexican original manufacturer.

The prevailing industrial landscape in Mexico is one of enclave economies. Highly productive, technologically state-of-the-art sectors do exist, but they are dominated by multinationals and generate few spillovers into the broader economy. The percent of foreign value added in Mexico’s exports has been estimated at anywhere from 48 percent to 69 percent, depending on the methodology. In any case, the country consistently has one of the highest shares of foreign value-added in its exports, suggesting a lack of competitive domestic suppliers.

So while the overall figures for industrial production might look good, they hide huge disparities among sectors and regions.

China, by contrast, has been able to generate increasingly competitive domestic firms in a range of sectors that consistently upgrade their productive structure towards higher-technology exports. Public policies played a huge role in this success. The Chinese government offers a variety of incentives and subsidies for domestic industries, as well as imposing requirements for foreign companies to form joint ventures with local firms, transfer technology, and source a significant share of their imports from domestic firms.

MexiCan’t touch this

These policies are, unsurprisingly, denounced by Western governments and companies as violating the norms of the open competition enshrined in the WTO. Moreover, they are policy options generally unavailable to Mexico since the signing of NAFTA in 1993. The agreement goes beyond WTO disciplines in prohibiting requirements on foreign investors that have helped China capitalize on its influx of FDI to ensure its economic competitiveness goes beyond mere cost advantages.

Let’s talk about you and me

So what does this mean for the promised reset of Mexico-China relations? Mexico should use its relationship with China to further its own efforts at promoting productivity and innovation. In the past, bilateral relations have failed to get off the ground, partly due to the Mexican government’s fixation on its trade deficit with China.

This obsession is short-sighted. For one, many Chinese products end up being transformed into Mexican exports to the US market, so clamping down on imports would hurt some Mexican producers. In addition, there is the issue of trade in value-added, which means that any one bilateral deficit or surplus does not capture the full complexity of the commercial exchange.

More importantly, the fact that Mexico is a strategic market for China represents an opportunity. The economic relationship between the countries has evolved from the story of cheap Chinese imports flooding Mexico’s market. Increasingly, Chinese companies in industries such as automobiles, electronics, and white goods seek to stake a claim on Mexico’s large consumer market and participate in production chains that link Mexico with the US.

Furthermore, China would certainly be interested in seizing any opportunities for foreign participation in Mexico’s oil sector that an anticipated energy reforms would create. To date, however, Chinese direct investment in Mexico has been meager, totaling around US$430mn between 2001 and 2012.

Mexico should take a page from the Chinese playbook and leverage the allure of its market to ensure that Chinese investments bring gains to the wider economy in the form of technology transfer and partnerships with domestic firms.

The Chinese, more than anyone, should appreciate the value of this approach.

Oh no Xi didn’t

Theodore Kahn is a researcher and analyst on trade and investment in Latin America. He has consulted for several international organizations and NGOs in the region and in Washington DC

Pingback: The Piñera Presidency: A Most Successful Failure | No Se Mancha

Pingback: After the ‘Golden Years,’ what next for Latin America? | No Se Mancha

Pingback: PEMEX Reform: The Final Frontier | No Se Mancha

Pingback: The Other Side of the Eike Batista Case | No Se Mancha

Pingback: Enrique’s PEMEX Plan | No Se Mancha

Really adore reading your site. Do you have any

specific tips about how to set up one.