Theodore Kahn on why the China-Latin America relationship disappoints.

Chinese investment in Latin America: still a one-trick pony

Chinese investment in Latin America has been back in the news recently. Two Chinese companies, PetroChina and CNOOC, were among the winning consortium in Brazil’s much-hyped Libra oil field auction last month. Then last week, PetroChina announced it would snap up $2.6 billion worth of Peruvian oil and gas fields from its new partner, Petrobras.

So has that long-promised wave of Chinese investment finally arrived? Don’t hold your breath.

Back in 2010, with most of the region riding out the Great Recession on China’s commodity-hungry coattails, the moment felt right for an influx of Chinese capital to complement booming trade and usher in a brave new era of so-called South-South cooperation.

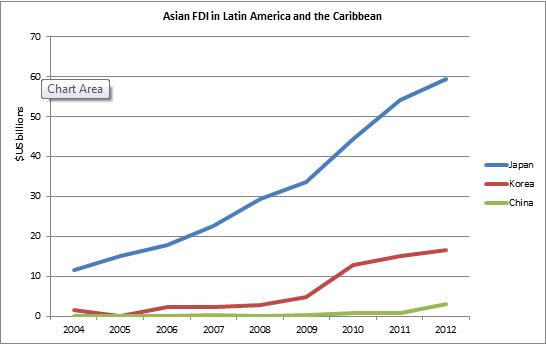

In that year, Chinese investment, which had been a mere trickle to date, finally seemed to arrive in significant quantities. According to ECLAC, some US$ 15 billion of investment flowed into the region in 2010.

From trains in Argentina, to copper in Peru to just about everything in Brazil, China’s promised billions were on the mind of governments throughout the region.

Unfortunately, the large majority of this investment never happened. It turns out it’s quite easy to sign an MoU signaling your intention to invest billions in a major infrastructure project; negotiating a deal agreeable to both sides, mustering the financing, and actually executing it is a different matter.

That’s how you get figures such the one reported earlier this year by the Brazil-China Business Council, which found that only one-third of announced Chinese investments in Brazil between 2007 and 2012 materialized; that translates into around US$ 44 billion left on the table.

Reporters from Reuters recently followed up on several proposed multi-billion dollar projects—one to build a railroad in Western Brazil and another for a soy processing facility—that have gone nowhere since being announced in 2010.

The result of all this is that official FDI statistics from China’s Ministry of Commerce show investment in Latin America has been a measly US$ 5.7 billion since 2006. This figure, chump change compared to global FDI flows, does not account for investment routed through Hong Kong, the Caribbean, or other tax havens. But it clearly shows that Chinese investment has been a major disappointment, especially in light of wildly inflated investment announcements.

In addition to the quantity of flows, the composition of Chinese investment provides further cause for disappointment. Chinese companies have been more than willing to snatch up natural resources, as the recent oil deals show.

Meet the new boss…

What they have not been so willing to do is make investments that would increase the capital stock or create value-added activities in the region. Those rail and road networks that would boost the region’s dilapidated transport infrastructure? Port upgrades? Nada.

Data from the Heritage Foundation’s China Investment Tracker back this up. Despite some recent interest in banks and other financial services, resources are basically the name of the game: a full 85% of China’s investments in the region since 2005 have been in oil, mining, or agriculture.

Not surprisingly, Chinese companies, most of them state-owned, are more interested in responding to their country’s massive resource requirements than entertaining Latin American pipe dreams (still alive and well, it turns out) about China’s massive reserves underwriting the region’s chronic infrastructure deficit.

As a result, the region’s business with China remains a one-dimensional affair: the commodities-for-manufacturing pattern dominates trade, and investment (to the extent that there is any) reinforces that trend.

Japan: Recipe for success?

The contrast with Japan, that other Asian giant, is noteworthy. Japan, despite its comparatively low profile, is by far the biggest Asian investor in the region. What’s more, its FDI is spread nearly equally across the primary, manufacturing, and services sectors: a recent study by the IDB on the region’s economic ties with Japan reports that 34% of Japanese FDI in the region has gone into manufacturing activities with another 35% directed to services.

Despite its low profile, Japan is far and away the largest Asian investor in LAC

In Mexico, Japanese car companies are building (and designing) next-generation electric cars. In Brazil, Hitachi is opening a research and innovation center to develop new information technologies tailored to the Brazilian market. And across the region, Japanese companies are investing in transport, renewable energy, and sanitation projects.

This was not always the case. In the early years of the Japan-LAC relationship, it was all about the resources. Japanese firms, unlike their Chinese counterparts, are not new arrivals in the region. In fact, Latin America was a major destination for Japanese outward FDI in the 1960s—by the middle of the decade, the region was absorbing a full quarter of Japan’s total foreign investment. Nearly all of that investment went towards securing supplies of the natural resources that Japan itself lacked but sorely needed to fuel its booming industry. Sound familiar?

Of course, the composition of Japanese FDI has since evolved—and diversified—as the figures cited above show.

So is it just a matter of a couple decades before China’s economic ties with the region start to look more like Japan’s? Perhaps. From one perspective, as China develops more globally competitive, privately-owned firms, who will look abroad for market rather than state-policy reasons, we might expect the next generation of Chinese firms to look to the Latin American market.

On the other hand, there is reason for some healthy skepticism. For Chinese firms, the domestic market is likely to become increasingly enticing in the coming years. This was most certainly not the case for Japanese firms, who have doubled down on Latin America over the past decade. When your domestic market is mature, saturated, and hobbled by deflation, the Latin American middle class seems like a good bet.

With consumers like these at home, why bother with Latin America?

But when you’re home market contains around a fifth of the world’s population, some 350 million of whom are likely to join the middle class in the coming decades, why bother with a suddenly anemic Latin America?

Besides the natural resources, of course.

Theodore Kahn is a PhD candidate at the Johns Hopkins School of Advanced International Studies. He has consulted for various international organizations and NGOs in Latin America and in Washington DC and previoulsy worked as a reporter in Argentina and Chile. Follow him on twitter: @TheoAKahn

Recently by Theodore

Brazil: Why the Protests Didn’t Sink Dilma

Mexico: Reforming Ain’t Easy

TPP and the Pacific Alliance: Two Visions of Asia-Latin America Trade

More on Latin America-Asia:

Uncle Sam’s Pacific Alliance Strategy (Samuel George)

Mexico-China Relations: Flipping the Script? (Theodore Kahn)

Pingback: How Deep are China’s Investments in the Carribbean? | The Peking Review

Pingback: Mexico’s Energy Reforms—We Ain’t Seen Nothing Yet | No Se Mancha

Pingback: Brazilian Bonds: Hot or Not? | No Se Mancha